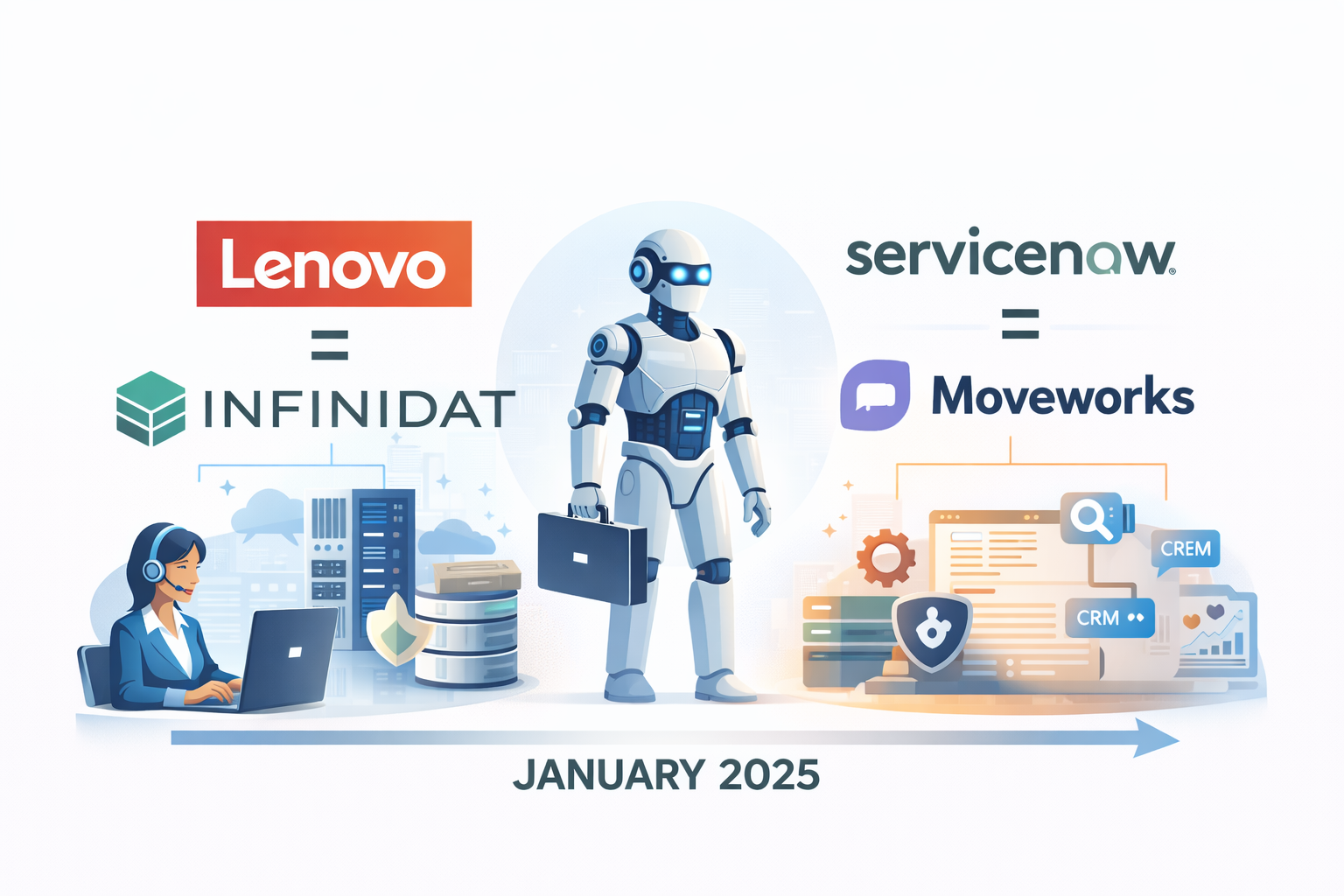

While technology executives debate AI strategy, Lenovo acquired Infinidat in January 2025 for estimated $1.5B to gain high-end AI-optimized storage while ServiceNow acquired Moveworks for $2.85B to embed agentic AI assistants into workflows through strategic AI M&A enterprise consolidation. This isn’t just acquisition activity, it’s systematic building of full-stack AI capabilities through comprehensive AI M&A enterprise.

Here’s what separates AI M&A winners from AI M&A followers: while your competitors develop AI capabilities organically, strategic acquirers weaponized AI M&A enterprise through Lenovo filling gaps in entry/mid-range portfolio for scalable AI workloads and ServiceNow creating unified search/self-service across CRM and ops through targeted AI M&A enterprise.

The result? CB Insights predicting agentic AI topping 2026 M&A targets at 30% of enterprise software deals with $500M-$5B valuations while December 2025’s $100B acquisition sprint sets premiums at 20-40% for defensible platforms, proving that AI M&A enterprise doesn’t just consolidate markets, it creates strategic competitive advantages through systematic AI M&A enterprise.

The AI M&A Enterprise Revolution That’s Redefining Technology Consolidation

When major technology companies execute billion-dollar acquisitions targeting AI infrastructure and capabilities, they’re not just buying companies, they’re fundamentally assembling full-stack AI platforms that individual development cannot match through strategic AI M&A enterprise.

Lenovo’s approach to AI M&A enterprise focuses on acquiring Infinidat’s high-end AI-optimized storage with cyber-resilient RAG data services that fill portfolio gaps through complementary AI M&A enterprise.

Their success with AI M&A enterprise demonstrates how strategic acquisitions enable rapid capability building versus organic development requiring years through accelerated AI M&A enterprise.

The transformation proves that AI M&A enterprise isn’t opportunistic deal-making, it’s systematic strategy to assemble AI stacks spanning storage, compute, data, and agentic layers through strategic AI M&A enterprise implementation.

How Strategic Acquirers Build AI Capabilities Through AI M&A Enterprise

Most technology companies attempt organic AI development, while strategic acquirers transformed capability building through AI M&A enterprise that purchases proven technologies and talent versus building from scratch.

The power of Lenovo’s AI M&A enterprise becomes evident through targeting Infinidat specifically for cyber-resilient RAG data services enabling enterprise AI workloads through purpose-driven AI M&A enterprise.

Their approach to AI M&A enterprise includes focusing on technologies filling specific gaps rather than acquiring broadly, ensuring strategic fit through targeted AI M&A enterprise.

When your AI M&A enterprise targets specific capability gaps with proven technologies, you achieve faster time-to-market than organic development through strategic AI M&A enterprise implementation.

The Agentic AI Focus Driving AI M&A Enterprise

Perhaps the most significant trend in AI M&A enterprise is ServiceNow’s $2.85B acquisition of Moveworks to embed agentic AI assistants into workflows, demonstrating that autonomous agents represent priority acquisition target through agentic AI M&A enterprise.

This agentic emphasis in AI M&A enterprise demonstrates how companies recognize that workflow automation through autonomous agents creates strategic value justifying premium valuations through valuable AI M&A enterprise.

ServiceNow’s AI M&A enterprise proves that agentic capabilities command high valuations because they transform business processes rather than just improving existing workflows through transformative AI M&A enterprise.

The organizations executing agentic-focused AI M&A enterprise will dominate enterprise automation while competitors struggle with assistant-level AI through strategic AI M&A enterprise.

The Unified Platform Strategy In AI M&A Enterprise

ServiceNow’s AI M&A enterprise includes creating unified search and self-service across CRM and operations by integrating Moveworks’ agentic capabilities through platform-building AI M&A enterprise.

This unification strategy through AI M&A enterprise demonstrates how acquisitions enable creating comprehensive platforms that isolated products cannot match through integrated AI M&A enterprise.

Their AI M&A enterprise approach recognizes that enterprise buyers prefer unified platforms over cobbling together multiple point solutions through consolidated AI M&A enterprise.

When your AI M&A enterprise builds unified platforms through strategic acquisitions, you achieve market positioning that fragment competitors cannot match through platform-focused AI M&A enterprise.

The CB Insights Predictions For AI M&A Enterprise

The forecasting dimension of AI M&A enterprise shows agentic AI topping 2026 targets at 30% of enterprise software deals with valuations ranging $500M-$5B through projected AI M&A enterprise.

This prediction about AI M&A enterprise demonstrates that autonomous agent capabilities will drive majority of enterprise software acquisition activity through agentic AI M&A enterprise.

CB Insights’ AI M&A enterprise forecasts include edge AI and healthcare AI following agentic as priority targets, showing multiple AI categories attracting acquisition interest through diversified AI M&A enterprise.

The market analysts’ AI M&A enterprise predictions suggest that companies planning acquisitions should focus on agentic, edge, and healthcare AI through strategic AI M&A enterprise.

The Valuation Premiums In AI M&A Enterprise

The pricing dynamics of AI M&A enterprise show December 2025’s $100B acquisition sprint setting premiums at 20-40% for defensible platforms amid scarcity through expensive AI M&A enterprise.

This premium level in AI M&A enterprise demonstrates that acquirers pay substantially above market multiples for AI capabilities with defensible competitive positions through valued AI M&A enterprise.

Their AI M&A enterprise includes examples like Palo Alto-CyberArk $25B deal showing that large-scale acquisitions command premium pricing through costly AI M&A enterprise.

When your AI M&A enterprise faces 20-40% premiums, strategic fit and defensibility become critical to justify high valuations through selective AI M&A enterprise.

The Healthcare AI Opportunity In AI M&A Enterprise

The sector-specific AI M&A enterprise includes healthcare AI targeting drug discovery and trials with CB Insights predicting 30% volume rise and $300M-$5B valuations through medical AI M&A enterprise.

This healthcare focus in AI M&A enterprise demonstrates how AI applications with clear ROI like accelerated drug discovery attract substantial acquisition interest through proven AI M&A enterprise.

Their AI M&A enterprise approach includes FDA-cleared healthcare AI plays exploding as outcomes prove return on investment through validated AI M&A enterprise.

The healthcare AI M&A enterprise represents particularly attractive targets because regulatory clearance creates barriers protecting acquired capabilities through defensible AI M&A enterprise.

The Full-Stack Consolidation Through AI M&A Enterprise

The strategic pattern in AI M&A enterprise involves consolidating AI stacks including storage, compute, data, and agentic layers to enable full-stack AI at scale through comprehensive AI M&A enterprise.

This stack consolidation through AI M&A enterprise demonstrates that competitive advantage requires controlling entire AI infrastructure rather than just application layer through complete AI M&A enterprise.

Lenovo’s AI M&A enterprise exemplifies this by acquiring storage infrastructure that complements existing compute capabilities through systematic AI M&A enterprise.

When your AI M&A enterprise builds complete stacks through strategic acquisitions, you achieve platform control that single-layer competitors lack through comprehensive AI M&A enterprise.

The Cyber M&A Predictions Within AI M&A Enterprise

The cybersecurity dimension of AI M&A enterprise includes predictions for 15-20 deals over $1B as companies acquire AI-powered security capabilities through cyber-focused AI M&A enterprise.

This cyber emphasis in AI M&A enterprise demonstrates how security represents priority acquisition category given AI’s role in threat detection and response through protective AI M&A enterprise.

Their AI M&A enterprise includes cyber-resilient capabilities like Infinidat’s RAG data services becoming acquisition targets for storage security through resilient AI M&A enterprise.

The cybersecurity AI M&A enterprise represents particularly active category because AI transforms both offensive and defensive capabilities through transformative AI M&A enterprise.

The Pharma M&A Spike In AI M&A Enterprise

The pharmaceutical AI M&A enterprise includes predicted spikes as drug companies acquire AI capabilities for discovery and development acceleration through pharma-focused AI M&A enterprise.

This pharmaceutical activity in AI M&A enterprise demonstrates how AI’s proven ability to accelerate drug timelines makes capabilities highly valuable to traditional pharma through valuable AI M&A enterprise.

Their AI M&A enterprise approach includes targeting AI platforms with FDA validation showing that regulatory approval creates acquisition premiums through validated AI M&A enterprise.

When pharmaceutical AI M&A enterprise accelerates, traditional drug companies recognize that AI acquisition provides faster capability than internal development through strategic AI M&A enterprise.

The Edge AI Opportunities In AI M&A Enterprise

The deployment-focused AI M&A enterprise includes edge AI targeting latency-sensitive and privacy-critical applications as secondary priority after agentic AI through edge-focused AI M&A enterprise.

This edge emphasis in AI M&A enterprise demonstrates how deployment architecture becomes acquisition driver when applications require local processing through distributed AI M&A enterprise.

Their AI M&A enterprise recognizes that edge AI enables use cases impossible with cloud-only approaches, creating defensible positions through specialized AI M&A enterprise.

The edge AI M&A enterprise represents growing category as IoT and real-time applications require on-device intelligence through edge-focused AI M&A enterprise.

The Strategic Implementation Lessons From AI M&A Enterprise

The 2025 AI M&A enterprise activity provides crucial insights for technology companies considering acquisitions. First, target specific capability gaps like storage or agentic workflows rather than broad technology plays through focused AI M&A enterprise.

Second, recognize that agentic AI commands premium valuations because autonomous agents transform workflows beyond simple automation through valued AI M&A enterprise.

Third, build full-stack capabilities through systematic acquisitions consolidating storage, compute, data, and application layers through comprehensive AI M&A enterprise.

Fourth, expect 20-40% premiums for defensible platforms with clear competitive moats in priority categories through expensive AI M&A enterprise.

The Future Belongs To AI M&A Enterprise Leaders

Your technology company’s capability transformation is approaching through AI M&A enterprise strategies that will define competitive positioning. The question is whether your organization will acquire strategically to build AI stacks or struggle with organic development.

AI M&A enterprise isn’t just about buying companies, it’s about strategic capability assembly that fundamentally changes competitive positioning by consolidating technologies spanning infrastructure through applications through systematic acquisitions that accelerate time-to-market.

The time for strategic AI M&A enterprise implementation is now as CB Insights predicts 30% of enterprise software deals targeting agentic AI with $500M-$5B valuations. The organizations that act decisively will establish platform advantages while competitors attempt organic development that cannot match acquisition speed.

The evidence from Lenovo-Infinidat $1.5B and ServiceNow-Moveworks $2.85B proves that comprehensive AI M&A enterprise works for building full-stack capabilities while CB Insights’ predictions validate that agentic AI will dominate 2026 acquisition activity. The only question remaining is whether your executive team has the vision to implement systematic AI M&A enterprise before competitors assemble insurmountable platform advantages through strategic acquisitions.